Last updated: 9 May 2026 | Reviewed against official UK guidance where available | Budgeting and Money Tips

Use the calculator as an estimate based on the balance, rate, tax band and time period you enter. GOV.UK says the Personal Savings Allowance is up to £1,000 for basic-rate taxpayers, £500 for higher-rate taxpayers and £0 for additional-rate taxpayers; the starting rate for savings can also apply depending on income.

Table of Contents

- How to Use This Savings Interest Calculator

- How Savings Interest Works in the UK

- Tax on Savings Interest: The Complete 2026/27 Guide

- Worked Examples: Calculating Your Savings Interest and Tax

- After-Tax Savings Rates by Income Tax Band (2026/27)

- The Bank of England Base Rate and Your Savings

- 7 Ways to Maximise Tax-Free Savings in 2026/27

How to Use This Savings Interest Calculator

Enter your savings balance, the annual interest rate your account pays, your income tax band and the period you plan to save for. The calculator estimates gross interest, how much may fall within your Personal Savings Allowance, any possible tax on the remainder, and an estimated net interest figure. The effective rate after tax is particularly useful: it lets you compare a taxable account against a cash ISA on a genuine like-for-like basis.

Toggle the ISA switch if your money is held in any type of ISA. In that case no tax applies and the PSA figures become irrelevant. Results update in real time as you change any input, so you can run multiple scenarios and compare accounts without doing any arithmetic yourself.

This calculator uses the official 2026/27 HMRC tax bands, Personal Savings Allowance rates and starting rate for savings thresholds. All figures are cross-referenced with GOV.UK guidance and updated for the current tax year.

A common misconception is that banks deduct tax from your savings interest before paying it. Since April 2016, all UK banks and building societies pay interest gross without any tax deducted. HMRC collects any tax owed by adjusting your PAYE code automatically. If you are a basic rate taxpayer earning under 1,000 in savings interest, you owe nothing at all thanks to the Personal Savings Allowance.

How Savings Interest Works in the UK

When you deposit money in a savings account, the bank or building society pays you interest as a reward for lending them your funds. That interest is calculated as a percentage of your balance and is typically quoted as an Annual Equivalent Rate (AER). Understanding the difference between the figures quoted and how interest is actually taxed is the first step to maximising what you keep.

AER Versus Gross Rate

Most savings accounts quote two figures: the gross rate and the AER. The gross rate is the contractual annual rate before compounding is taken into account. The AER factors in how often interest is paid during the year (monthly, quarterly or annually) and converts everything into a single comparable annual figure. When a bank pays interest monthly and you leave it in the account, the interest earns further interest, so the AER will be slightly higher than the gross rate. When comparing accounts, always use the AER: it reflects the true return you will receive over a full year if the rate does not change.

Simple Versus Compound Interest

Simple interest is calculated only on your original deposit. Put £10,000 in an account at 4.5% simple interest and you earn £450 per year, every year. Compound interest is calculated on your growing balance, including previously credited interest. Leave £10,000 for five years at 4.5% compounding annually and you end up with £12,461 rather than £12,250. The gap widens the longer you save. Our calculator uses simple annual interest for clean, directly comparable figures, which is how the majority of easy-access accounts and fixed-rate bonds work in practice.

Tax on Savings Interest: The Complete 2026/27 Guide

Since April 2016, UK banks and building societies have paid savings interest gross, without deducting any tax at source. It is now your responsibility to ensure any tax owed is paid. Fortunately, most savers pay no tax at all, thanks to the Personal Savings Allowance. For a comprehensive breakdown of every rule and edge case, read our full guide to tax on savings interest.

The Personal Savings Allowance in 2026/27

The Personal Savings Allowance (PSA) gives most savers a tax-free band of interest each year. The amount depends on your income tax band:

- Non-taxpayer or low income: GOV.UK says your Personal Allowance, starting rate for savings and Personal Savings Allowance may cover some or all savings interest, depending on your other income.

- Basic rate taxpayer (income £12,571 to £50,270): The first £1,000 of savings interest per tax year is tax-free.

- Higher rate taxpayer (income £50,271 to £125,140): The first £500 of savings interest per tax year is tax-free.

- Additional rate taxpayer (income over £125,140): No Personal Savings Allowance. All savings interest is subject to income tax at 45%.

The PSA applies per person, not per account. If you hold three savings accounts that together pay £1,200 in interest and you are a basic rate taxpayer, £1,000 is covered by the PSA and only £200 is taxable.

The Starting Rate for Savings

There is a lesser-known relief called the starting rate for savings that can extend your tax-free interest entitlement significantly. If your non-savings income (wages, pension, rental income) is below £17,570, you may qualify for up to £5,000 of savings interest taxed at 0%. The starting rate band reduces by £1 for every £1 of non-savings income above the £12,570 Personal Allowance. Someone with non-savings income of exactly £12,570 gets the full £5,000 starting rate; someone with £15,000 of non-savings income gets £2,570.

This relief is particularly valuable for retirees living on a modest pension, people working part-time, or anyone taking a career break. To claim, contact HMRC or complete form R40 to reclaim any tax already deducted. You can also register via GOV.UK to receive interest gross.

ISA Interest Is Always Tax-Free

Any interest, dividends or gains generated inside an ISA are completely exempt from UK income tax and capital gains tax. The ISA wrapper removes savings income from all tax calculations permanently. You do not need to declare ISA income on a Self Assessment return, and it does not consume any of your Personal Savings Allowance. The annual ISA allowance for 2026/27 remains £20,000 per person.

For a full breakdown of the rules covering cash ISAs this year, read our article on Cash ISA rules for 2026, and for the wider picture including possible future changes see our ISA allowance guide.

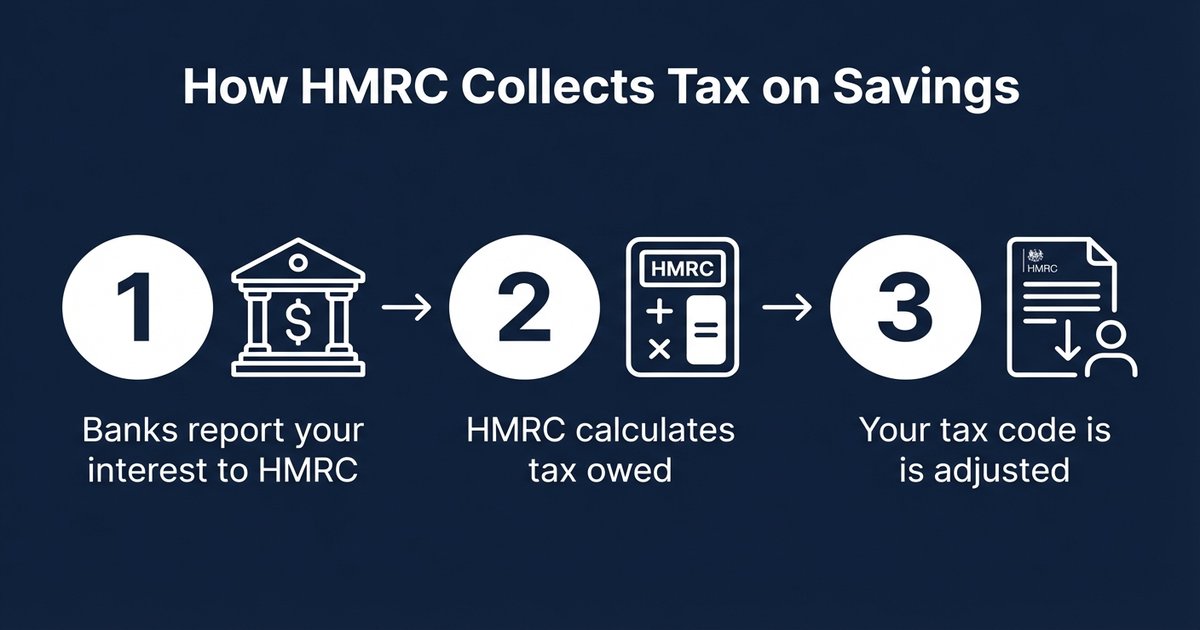

How HMRC Collects Tax on Savings Interest

If your savings interest exceeds your Personal Savings Allowance, HMRC will normally collect the tax automatically by adjusting your PAYE tax code for the following tax year. Banks and building societies are required to report the interest paid to each customer to HMRC annually. HMRC cross-references this against your income record, calculates the tax owed, and reduces your personal allowance in your code to recover the correct amount through future wages or pension payments.

You do not need to contact HMRC proactively. However, if you are self-employed, not in PAYE employment, or your total untaxed income (including savings interest) exceeds £10,000, you must file a Self Assessment tax return and declare your savings income there. Check your tax code notice every April to confirm HMRC has used the correct interest figure: inaccuracies are more common than most people realise.

Premium Bonds: Prizes Are Always Tax-Free

Premium Bonds, issued by NS&I and backed by the Treasury, do not pay interest. Instead they enter you into a monthly prize draw where all prizes from £25 to £1,000,000 are completely tax-free. Prizes do not count towards your Personal Savings Allowance and do not affect your tax code. You can hold up to £50,000 in Premium Bonds per person. For higher and additional rate taxpayers, the tax-free nature of prizes makes the effective return more competitive than the headline prize fund rate suggests when compared to a taxable savings account at the same rate.

Worked Examples: Calculating Your Savings Interest and Tax

Example 1: Basic Rate Taxpayer With £20,000

Emma is a teacher earning £36,000 a year, placing her in the basic rate band. She has £20,000 in a one-year fixed-rate bond paying 4.8% AER.

- Gross interest: £20,000 x 4.8% = £960

- Personal Savings Allowance: £1,000

- Taxable interest: £0 (£960 is below the £1,000 allowance)

- Tax owed: £0

- Net interest: £960

- Effective rate after tax: 4.80% (unchanged, no tax applies)

Emma pays nothing in tax because her annual interest stays within her PSA. She keeps every penny of the £960.

Example 2: Higher Rate Taxpayer With £50,000

David is a senior manager earning £80,000 per year. He has £50,000 in an easy-access savings account paying 4.5% AER.

- Gross interest: £50,000 x 4.5% = £2,250

- Personal Savings Allowance: £500

- Taxable interest: £2,250 – £500 = £1,750

- Tax owed: £1,750 x 40% = £700

- Net interest: £2,250 – £700 = £1,550

- Effective rate after tax: £1,550 / £50,000 = 3.10% p.a.

HMRC will adjust David’s PAYE code in the following tax year to recover the £700. His apparently attractive 4.5% account actually delivers only 3.10% after tax, a significant reduction.

Example 3: ISA Versus Taxable Account for a Higher Rate Taxpayer

Rachel is a higher rate taxpayer with £25,000 to place in savings. She is comparing two options:

- Option A: Taxable easy-access account at 4.6% AER

- Option B: Cash ISA at 4.2% AER (completely tax-free)

Option A calculation: Gross interest = £1,150. PSA covers £500. Taxable interest = £650. Tax at 40% = £260. Net interest = £890. Effective rate = 3.56%.

Option B calculation: Gross interest = £1,050. No tax. Net interest = £1,050. Effective rate = 4.20%.

Despite the lower headline rate, the ISA pays Rachel £160 more per year. This example shows why comparing gross rates alone is misleading for higher and additional rate taxpayers. The after-tax effective rate is the only number that matters.

After-Tax Savings Rates by Income Tax Band (2026/27)

The table below shows the effective after-tax return from a savings account paying 4.5% AER, at different balances and tax bands. Figures assume interest is paid and calculated over one year.

| Tax Band | PSA | Tax Rate | Effective Rate on £10,000 | Effective Rate on £50,000 |

|---|---|---|---|---|

| Non-taxpayer | Unlimited | 0% | 4.50% | 4.50% |

| Basic rate (20%) | £1,000 | 20% | 4.50% (within PSA) | 3.96% |

| Higher rate (40%) | £500 | 40% | 3.30% | 2.76% |

| Additional rate (45%) | £0 | 45% | 2.48% | 2.48% |

Note: the basic rate figure at £10,000 assumes the £450 gross interest stays within the £1,000 PSA, so no tax is deducted. At £50,000, interest of £2,250 exceeds the £1,000 PSA, leaving £1,250 taxable at 20% (£250 tax), giving a net of £2,000 on £50,000, which equals 4.00%. The 3.96% figure accounts for rounding. Use the calculator at the top of this page for precise figures based on your actual balance and rate.

The Bank of England Base Rate and Your Savings

Savings rates across the UK are heavily influenced by the Bank of England base rate, set by the Monetary Policy Committee at eight scheduled meetings per year. When the base rate rises, banks generally pass some of that increase on to savers, though rarely the full amount and often with a delay. When it falls, savings rates typically follow quickly.

Fixed-rate bonds lock in a rate at the point you open the account, which is valuable when rates are expected to fall. Easy-access accounts give flexibility but the rate can be reduced at any time. Keeping an eye on base rate decisions and comparing accounts regularly is worthwhile, particularly for larger balances where even a 0.1% difference represents meaningful money over a year.

7 Ways to Maximise Tax-Free Savings in 2026/27

1. Use Your ISA Allowance Every Year

The most reliable way to shelter savings interest from tax is to use your £20,000 annual ISA allowance. Interest inside an ISA is tax-free forever and never needs to be declared to HMRC. Unlike the Personal Savings Allowance, the ISA is not affected by changes to your income or tax band. Once money is inside an ISA, it remains sheltered regardless of how large the returns grow.

2. Split Savings Between Partners

If you are married or in a civil partnership, each of you has a separate Personal Savings Allowance and a separate £20,000 ISA allowance. A basic rate couple can shield up to £2,000 of combined savings interest through their PSAs, plus up to £40,000 of new savings per year inside their ISAs. Moving savings to the partner with the lower tax band, or ensuring both allowances are fully used, can substantially reduce the household tax bill on savings.

3. Claim the Starting Rate for Savings If You Qualify

If your non-savings income is below £17,570, you may be entitled to the starting rate for savings, which taxes up to £5,000 of interest at 0%. This is over and above the Personal Savings Allowance. Retirees, part-time workers and people taking a break from work often qualify without realising it. Use form R40 to reclaim any overpaid tax from up to four previous tax years.

4. Consider Premium Bonds for Large Balances

For higher and additional rate taxpayers with significant savings, Premium Bonds offer tax-free prizes with no risk to capital and full Treasury backing. The effective return depends on the prize fund rate and the statistical distribution of wins, but the tax-free nature of prizes makes them competitive with taxable savings accounts at similar stated rates, particularly for additional rate taxpayers who lose 45p in every pound of interest above their PSA.

5. Use a Flexible ISA as Your Emergency Fund

Flexible ISAs allow you to withdraw and replace money in the same tax year without losing your allowance. This removes the usual trade-off between keeping an accessible emergency fund and maximising ISA contributions. You can keep three to six months of expenses inside a flexible cash ISA, earning tax-free interest, and replenish any withdrawals before April without any tax consequence.

6. Stagger Fixed-Rate Bond Maturities Across Tax Years

If a large fixed-rate bond matures and pays all its interest in a single tax year, the full amount counts towards your PSA in that year. If you also have other savings accounts, you may exceed your allowance simply through timing. Opening bonds that mature in different tax years smooths your interest income, keeps you within the PSA more consistently, and reduces unnecessary tax bills.

7. Check Your Tax Code Every April

HMRC uses bank-reported interest data to adjust your PAYE code, but errors are common. Banks sometimes report the wrong figure, use the wrong tax year, or miss accounts that were opened mid-year. Check your coding notice every April and compare the interest figure HMRC has used against your actual savings statements. If the figure is wrong, contact HMRC directly. Overpaid tax can be reclaimed but you need to act within four years of the end of the relevant tax year.

- GOV.UK: Tax on savings interest

- GOV.UK: Individual Savings Accounts

- Bank of England: Bank Rate

- FSCS: Deposit protection limits

Rules, rates and provider terms may change. Check official sources before making financial decisions.

Before you act: savings checks

Use this section as a final check before applying, claiming, switching, transferring money or relying on a figure. Rules, rates and provider terms can change, so verify the current position with the linked official sources.

| Decision point | What to check | Source to verify |

|---|---|---|

| Tax position | Check Personal Savings Allowance, ISA allowance and whether interest will be taxable for your circumstances. | GOV.UK: tax on savings interest GOV.UK |

| Access | Compare withdrawals, notice periods, maturity rules, penalties and whether the rate is fixed or variable. | GOV.UK: Individual Savings Accounts Provider terms |

| Protection | Check FSCS or NS&I protection and whether brands share one banking licence. | FSCS: deposit protection FSCS / NS&I |

- Monthly Interest Savings Accounts UK 2026: Best Rates and Who They Suit

- Fixed Rate Bond vs Cash ISA: Which Pays More After Tax in 2026/27?

- Cash ISA Rule Changes 2026: What the New Limits Mean for Your Savings

- Claiming Premium Bonds After a Death in 2026: What to Do When NS&I Delays Your Payout

- Junior ISA vs Savings Account: Which Is Better for Your Child’s Money in 2026?

Editorial note: this URL was flagged as a future merge candidate in the audit, but it has not been noindexed or redirected in this update.

Frequently Asked Questions

How is savings interest taxed in the UK?

Savings interest in the UK is subject to income tax at your marginal rate. Banks and building societies have paid interest gross since April 2016, without deducting tax at source. Most people pay no tax on their savings thanks to the Personal Savings Allowance (up to £1,000 for basic rate taxpayers, £500 for higher rate). Interest inside an ISA is completely tax-free. HMRC collects any tax due by adjusting your PAYE code, so no action is required from most employees and pensioners.

How much savings interest can I earn before paying tax in 2026/27?

It depends on your income tax band. Non-taxpayers with income below £12,570 pay no tax on any savings interest. Basic rate taxpayers (income £12,571 to £50,270) can earn up to £1,000 tax-free. Higher rate taxpayers (income £50,271 to £125,140) can earn up to £500 tax-free. Additional rate taxpayers (income over £125,140) have no allowance and pay 45% on all savings interest. Low earners may also qualify for up to £5,000 of additional tax-free interest through the starting rate for savings. All ISA interest is tax-free regardless of band.

Does ISA interest count towards my Personal Savings Allowance?

No. Interest earned inside any type of ISA, whether a cash ISA, stocks and shares ISA, Lifetime ISA or innovative finance ISA, does not count towards your Personal Savings Allowance. The two reliefs are completely separate. ISA income sits in a fully exempt wrapper and does not appear on your tax return or affect your PAYE code in any way.

What happens if I earn more than my Personal Savings Allowance?

Any savings interest above your PSA is taxed at your marginal rate: 20% for basic rate taxpayers, 40% for higher rate, or 45% for additional rate. HMRC will normally collect the extra tax by reducing your personal allowance in your PAYE code for the following tax year, meaning the tax is spread across your regular pay. If you complete a Self Assessment return, you declare the interest there and settle it through your annual bill. You do not need to contact HMRC in advance as the process is automatic for PAYE taxpayers.

Is interest on a joint savings account split between two people?

Yes. HMRC treats interest on a joint account as belonging equally to each account holder, unless both parties have made a written declaration of a different split. Each person receives half the interest and uses half their Personal Savings Allowance against it. If one holder is a non-taxpayer and the other is a higher rate taxpayer, moving savings into the non-taxpayer’s sole name can reduce the household tax bill considerably.

How does HMRC find out about my savings interest?

UK banks and building societies are legally required to report the interest paid to each customer to HMRC every year. HMRC matches this data against your National Insurance number and income record. For PAYE employees and pensioners, any tax owed is collected automatically through a code adjustment. You do not need to tell HMRC about your interest separately unless you file a Self Assessment return or your total untaxed income exceeds £10,000 per year.

Can I reclaim tax I have already paid on savings interest?

Yes. If you were a non-taxpayer or a low earner qualifying for the starting rate for savings and tax was deducted in error, you can reclaim it using form R40 for up to four previous tax years. Check GOV.UK or HMRC guidance before reclaiming tax or asking HMRC to correct your position. If you believe your PAYE code has overcharged you on savings interest, contact HMRC with your bank statements showing the correct interest figure and request a refund.

What is AER and why does it matter for savings calculations?

AER stands for Annual Equivalent Rate. It is a standardised calculation that shows what your return would be if interest were compounded and paid once a year. It accounts for how frequently the bank actually credits interest (monthly, quarterly, etc.) and converts everything to a single comparable annual figure. When a bank pays monthly interest that compounds, the AER will be slightly higher than the gross rate. Always use the AER when comparing accounts: it is the only figure that gives a true like-for-like comparison across different products and payment frequencies.

- UK Savings Interest Calculator 2026/27

- How to Use This Savings Interest Calculator

- How Savings Interest Works in the UK

- Tax on Savings Interest: The Complete 2026/27 Guide

- Worked Examples: Calculating Your Savings Interest and Tax

- After-Tax Savings Rates by Income Tax Band (2026/27)

MoneyWise UK provides information for general guidance only. This is not financial advice. Always consult a qualified financial adviser before making major financial decisions.